Every year, millions of American workers experience some form of short-term disability lasting six months or fewer. Imagine Bill, a dedicated worker temporarily sidelined by an unexpected surgery. Or Sarah, facing medical complications after giving birth. Or Jane, whose bout with pneumonia turned unexpectedly bad, resulting in hospitalization and an extended—but temporary—recovery.

In the face of these issues, all of these workers are likely left worrying about how to pay their bills. They’re far from alone in this experience; research shows that 5.6% of working Americans—nearly 10 million workers annually—experience a short-term disability each year. Worse, few of them are financially prepared for such a setback; nearly 40% of individuals have $1,000 or less in savings.

Enter short-term disability insurance - a lifeline for employees and a strategic advantage for employers.

What is Short-Term Disability?

But what is short-term disability, and why should it matter to employers? In essence, short-term disability insurance provides income protection for employees during temporary periods when they are unable to work due to medical conditions. It’s designed to help bridge the gap between the onset of a disability and the employee’s return to work or transition to long-term disability benefits if necessary.

Importantly, it benefits more than just workers. For employers, it’s a cornerstone of a supportive workplace culture that can make the employer more attractive to prospective hires and reduce turnover and certain costs.

Short-term disability plans vary enormously. Some states have specific statutory requirements, while most states leave it entirely up to the employer. Then, different plans will have different requirements for what qualifies for short term disability. As a result, exact coverages, options, costs, and eligibility requirements will vary according to the plan(s) purchased.

What Does Short-Term Disability Cover?

Short-term disability insurance covers a wide range of medical conditions that render an employee temporarily unable to work. What qualifies for short-term disability can include:

- Recovery from surgery, such as knee replacements or heart procedures.

- Injuries sustained in accidents, like fractures or burns.

- Illnesses that temporarily incapacitate an individual, including severe flu or pneumonia.

- Pregnancy-related conditions, such as complications before or after childbirth.

That last point is particularly noteworthy. Many employers (and employees) may not even realize that short-term disability insurance can potentially provide income replacement during post-childbirth recovery. Similarly, modern short-term disability plans also increasingly recognize the growing impact of mental health issues. Short-term disability mental health coverage typically includes conditions like severe depression, anxiety disorders, and post-traumatic stress disorder (PTSD), acknowledging that mental health challenges can be as debilitating as physical ones.

However, not all situations qualify for benefits. Pre-existing conditions may be excluded, and self-inflicted injuries or those resulting from illegal activities are typically not covered. Additionally, to qualify for short-term disability, employees must typically provide medical documentation from a healthcare provider confirming their inability to work due to the condition.

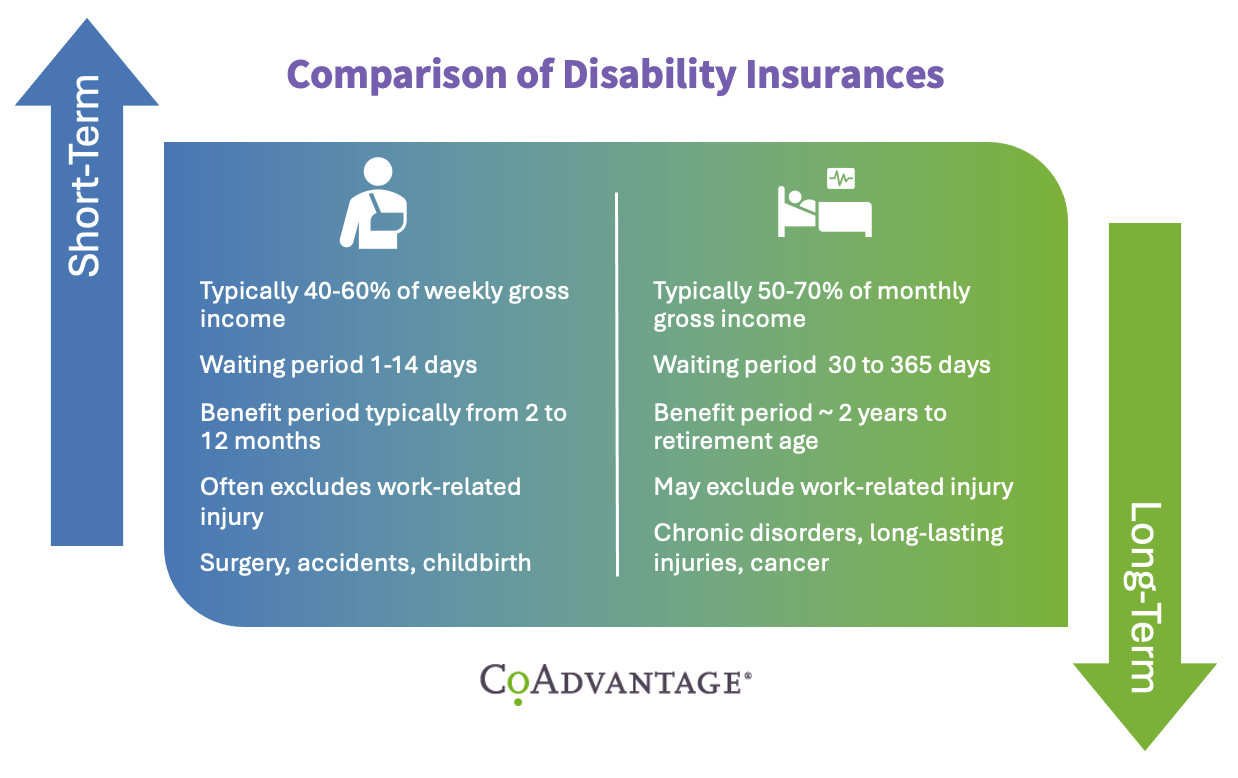

Benefit Amount and Duration

Most STD policies replace 40-60% of an employee's pre-disability income for a period of 9 to 26 weeks. That short duration is the principal difference between short-term and long-term disability coverage.

That said, it all depends on the policy. Some plans will go as high as 100% replacement value and last as long as a year. Virtually all policies, however, will have brief waiting periods—typically one to two weeks—before benefits begin, requiring employees to rely on sick leave or other resources in the interim.

Employers should carefully select plans that align with the needs of their workforce. Practically speaking, this means conducting a thorough analysis of the organization’s demographics, industry benchmarks, and employee feedback. For instance, employers might consider the average age of their workforce, the prevalence of roles that carry higher risks of injury, or the demand for maternity-related benefits.

Engaging with benefits consultants and/or surveying employees about their preferences can provide valuable insights for tailoring the policy effectively.

bvious why short-term disability insurance would be helpful for employees: it’s a financial safety net, ensuring workers can meet essential expenses while recovering from short-term issues. Moreover, the inclusion of short-term disability mental health coverage ensures that employees grappling with mental health challenges are not left behind, promoting a more inclusive and supportive workplace culture.

But it’s important to understand the short-term disability benefit offerings can also help employers, too.

Competitive Advantage

In a tight labor market, short-term disability insurance contributes to a competitive benefits package that can help employers stand out. While job seekers may not prioritize short-term disability specifically during their decision-making process, its inclusion as part of a broader set of benefits can differentiate your organization from competitors with more constrained offerings. And most offerings are more limited: according to the U.S. Bureau of Labor Statistics, short-term disability insurance is only available to approximately two out of every five civil workers. That gap is a prime opportunity for competitive differentiation in the labor market.

Reduced Turnover

Additionally, comprehensive benefits, including short-term disability, can help to reduce turnover by providing a financial safety net for employees facing temporary health challenges. In other words, it creates a bridge that allows employees to recover and return to work, rather than leave their jobs entirely because they were unable to recover or were forced to find other employment or financial support in the meantime. This stability not only retains skilled workers but also strengthens organizational resilience by minimizing disruptions caused by employee departures.

What Steps Should Employers Take?

1: Offer Short-Term Disability Coverage

Making short-term disability insurance part of the standard benefits package ensures broader access and is the first and foundational step of reaping its benefits for both the employer and employee. Then, provide clear, accessible information about the availability and benefits of this insurance to ensure employees realize the benefit is available to them and understand its value.

2: Update Benefits Language

Since modern short-term disability plans incorporate more than just obvious accidents and illnesses, including short term disability mental health issues, it’s important to ensure any relevant policies and training or onboarding materials are kept up to date. As HR Executive points out, “The outdated language in these benefits packages may also cause confusion about the benefits employers provide at no cost to help care for their employees.”

3: Get Help

Everything from selecting the right short-term disability plans for your workforce to updating policies requires understanding how these plans work—and what legal requirements they must follow. However, most employers retain pretty much all administration of disability-related benefits internally; only 21% outsource some or all such functions to an external administrator.

That makes this a prime area for improving compliance and sourcing short-term disability plans at lower cost by going through a PEO or other third-party partner. For example, you are likely to find more cost-competitive plans by going through a service like a PEO which can offer economy-of-scale pricing to even small and midsize businesses.

For more information about short-term disability coverage, how to source it cost-effectively, and how to integrate it into your total benefits package, contact us today or learn more about our benefits services. CoAdvantage is one of the nation’s largest Professional Employer Organizations (PEOs) and helps small to mid-sized companies with HR administration, benefits, payroll, and compliance.